News

Istanbul Chamber of Industry Announces “Türkiye’s Second Top 500 Industrial Enterprises-2020” Survey Results

- 06.07.2021

- News

Following the "ICI Türkiye's Top 500 Industrial Enterprises-2020” survey last month, the Istanbul Chamber of Industry ("ICI") has published the results of the “ICI Türkiye’s Second Top 500 Industrial Enterprises-2020” survey today.

As in previous years, this year’s survey of Türkiye’s Second Top 500 Industrial Enterprises (ICI Second Top 500) in 2020 has shown important results in terms of the current state and future of SMEs.

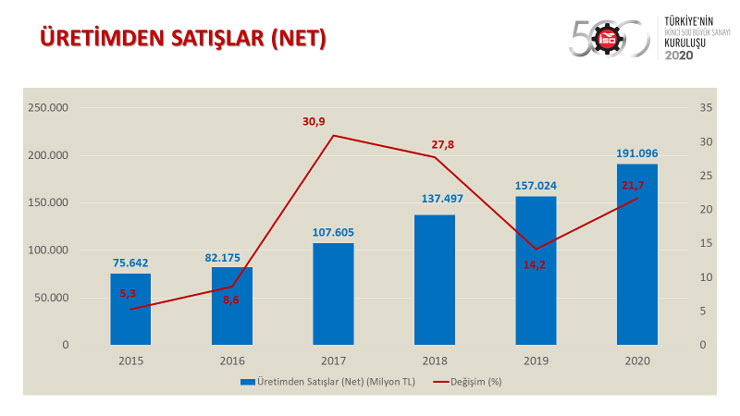

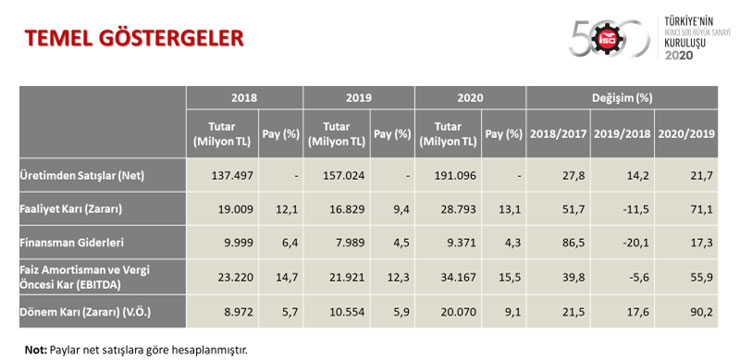

According to a statement by the Istanbul Chamber of Industry, the net sales of the ICI Second Top 500 rose by 21.7 percent to 191.1 billion Turkish lira from 157 billion Turkish lira in 2020.

ICI Chairman of the Board, Erdal Bahçıvan:

"OUR SMEs HAVE DEMONSTRATED THEIR READINESS TO STRENGTHEN THEIR PRODUCTION UNDER FAVORABLE FINANCING CONDITIONS"

“Since 1998, we have been consistently publishing the ICI 500, one of the most valuable works of our chamber, and the second of our ICI Second Top 500 surveys we have been doing since 1968.

The ICI Second 500 has demonstrated the general outlook of our industry as much as the ICI Top 500, and today, it is a work that becomes more important for us to draw a picture of the Turkish economy and industry.

ICI Second Top 500 reinforces its brand value with the participation of different industries and provinces each year. Compared to ICI Top 500, this study has specific features as it mainly covers companies with SMEs, and in the coming days, we believe that it will be examined with interest and will have a positive effect on the public opinion with its different results.

If I were to mention a few of these results; starting from the fact that the ICI Second Top 500 increased its production-based net sales by 6 percent in real terms, in a challenging year like 2020 with the pandemic, we are witnessing that it gives brighter than expected results in many areas such as exports, employment, profitability, financing expenses, technological structure, and R&D expenses.

At this point, I would like to point out the improvements in many profitability indicators, including sales profitability, asset profitability, operating profit and EBITDA performance. Among the reasons why we see the brightest data on the profitability in ICI Second 500 include supportive practices such as low commodity prices throughout the year, favorable credit conditions and low interest rates especially in the second half of the year, keeping the profit margins high by limiting the operating costs of the companies. We consider these developments to be promising, since it will cause a strong increase of 22 percent in the equity of ICI Second Top 500 companies.

Our SMEs' export performance differs greatly from that of Türkiye and our ICI Top 500 study. In this difficult year, there was a loss of exports in the ICI 500, as in the Turkish and industrial sectors. Therefore, the ICI Second Top 500 deserves all the credit for increasing its exports by 1.2 per cent. It should also be taken into account that the ICI Second Top 500's employment gain is faster than the ICI 500's, at 4.6 percent.

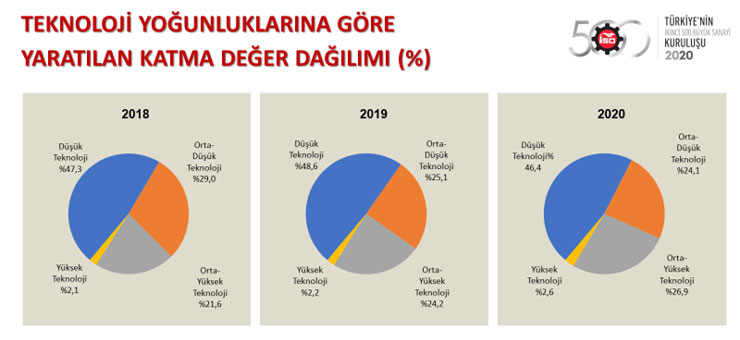

Another remarkable indicator for the future is the fact that the total share of medium-high and high technology-intensive industries in the ICI Second 500 companies increased by 3.1 points to 29.5 percent in 2020. Nevertheless, we must keep in mind that new investments and initiatives are needed to achieve the targeted advances in technology and value-added structure.

Of course, there are many indicators in the ICI Second Top 500 that need further improvement, especially in financial terms. For example, the distribution of current and non-current assets, resource structure, net foreign exchange position, public offering trends, desire and abilities to carry out R&D...

Finally, ICI Second Top 500 data show Turkish industry's readiness to strengthen the manufacturing force for healthy growth once the favorable financing conditions are found. This picture is also valuable in terms of demonstrating the significant improvement in the management skills of SMEs under difficult conditions in 2020. We hope these companies' performance is reflected to throughout Türkiye and that this positive outlook is sustained in the future as well. As we have always said, favorable financing is the most important factor in preserving the economy, production and dynamism of our country. When we look at the results of ICI Second Top 500 from this perspective, we need to further promote the strong potential of our SMEs."

After a considerable increase of 27.8% in 2018, net sales from the production of the ICI Second Top 500 decreased by 14.2 percent in 2019. In a year marked by pandemic conditions such as 2020 and with many companies experiencing shutdowns and production slowdown, it is noteworthy that net sales of the ICI Second Top 500 gained momentum after the fluctuations in domestic and foreign demand.

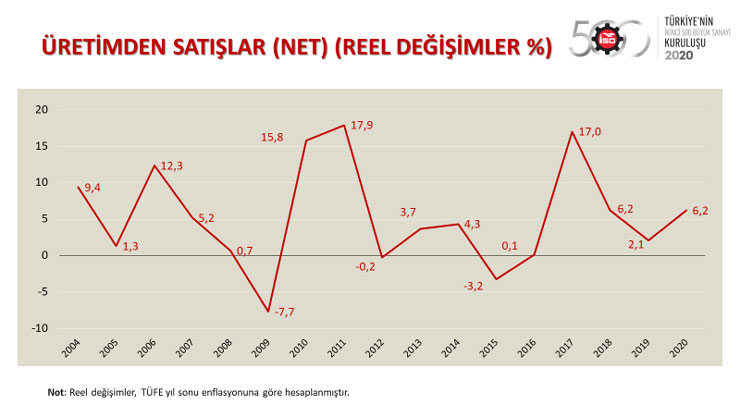

When we analyze the changes in the net sales of the ICI Second Top 500 by subtracting the CPI inflation, we saw strong real increases in 2017 and 2018 after the weak growth in the 2012-2016 period.

Even in a hard year like 2020, SMEs were successful in their production and marketing activities with their adaptable structures, as evidenced by the fact that production-based net sales of the ICI Second Top 500 increased by 6.2 percent in real terms. As you may recall, there was a limited real increase in net sales of the ICI 500, which was announced in May, by 0.6 percent.

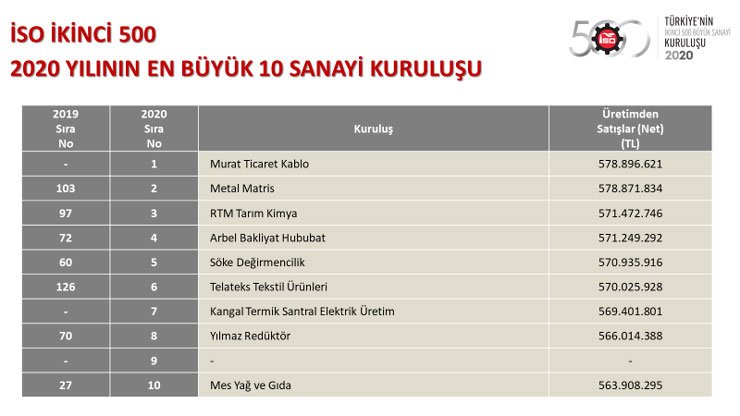

The top three companies of the ICI Second Top 500

Looking at the ranking of the ICI Second Top 500, based on production-based net sales, in 2020; Murat Ticaret Kablo took the first place with TL 578.9 million. It was followed by Metal Matrix with a slight difference of 578.9 million Turkish Lira, and RTM Agricultural Kimya as third with 571.5 million Turkish Lira.

This year, 119 new industrial enterprises entered the ICI's Second Top 500 list. Of these, 30 companies fell from ICI Top 500 to the ICI Second Top 500. Out of the ICI 1000 list, the number of new companies was 89 last year, while the number of companies that climbed to ICI Top 500 from the ICI's Second Top 500 list in 2019 was 39.

Companies that made production-based net sales in the band of TL 482.1 million and TL 201.2 million in 2019 were included in the ICI Second 500 list, and according to the 2020 results, this band was between TL 578.9 million and TL 251.6 million.

Looking at the results of ICI Second Top 500, which shows the check-up of Türkiye's SME-scale industrial structure, in 2020, a year marked by a severe pandemic, the success in production-based net sales appears in other indicators as well. For example, the ICI Second Top 500 indicates brighter results than expected in many parameters such as exports, technology intensity, employment, profitability, financing expenses, and R&D spending.

An examination of the value added distribution created by the ICI Second Top 500 based on their technology intensity indicates that even though low-tech industries had the highest share with 46.4 percent, the share of mid-to-high tech industries rose. This share increased by 2.7 percent to 26.9 percent in 2020, up from 24.2 percent in 2019.

The share of the high-tech industries rose slightly to 2.6 percent in 2020, up from 2.2 percent in 2019. On the other hand, the total share of mid-to-high and high-tech industries climbed by 3.1 percent to 29.5 percent in 2020, signalling a positive trend for the future.

The outbreak of 2020 caused a major contraction in global trade. Export markets remained closed to a large extent, especially in the first half of the year. Despite the improvement started in global trade in the second part of the year, Türkiye's total exports fell by 6.2 percent in 2020, as a result of the continuous negative effects of the epidemic, with industrial exports falling by 6.6 percent. The loss of exports in the ICI 500 was 12.8 percent, higher than that of the Turkish and industrial sectors.

On the other hand, the exports of the ICI Second Top 500 increased by 1.2 percent to $9.9 billion in the same year. Consequently, the share of the ICI Second Top 500 in Türkiye's total exports was 5.9 percent and its share in industrial exports was 6.1 percent, both indicating an increase of 0.5 points compared to 2019.

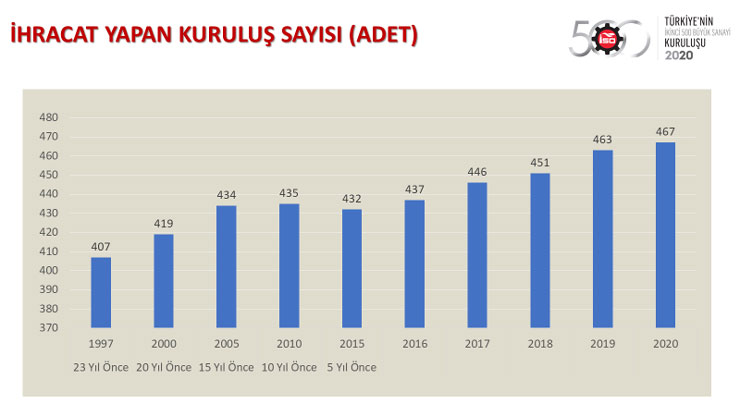

Another important development on the export side is the upward trend in the number of exporting companies. The number of companies exporting to the ICI Second Top 500 rose from 407 in 1997 to 467 in 2020, which surpassed the 450s band in the last three years. This is a really positive development since it demonstrates that the tremendous progress of ICI Second Top 500 companies in expanding their international markets. In addition, the ICI Second 500 companies that do not export seem to find it increasingly difficult to find a place in this ranking, just as companies in ICI Top 500.

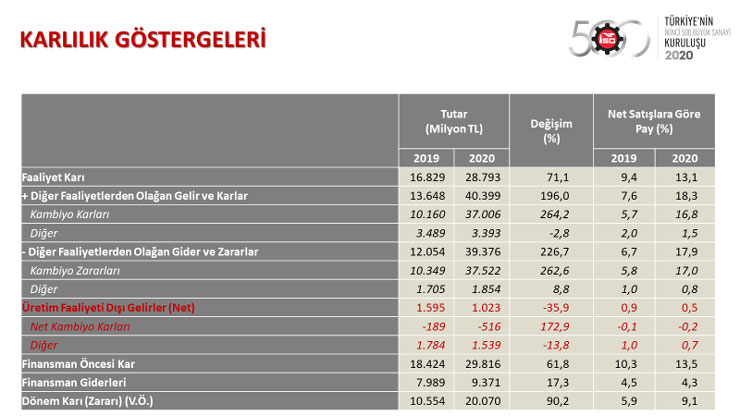

In 2020, it is seen that the ICI Second Top 500 exhibited a high performance especially in terms of profitability. Operating profit rose 71.1 percent to TL 28.8 billion in 2020, up from TL 16.8 billion in 2019. Accordingly, the operating profit ratio went up by 3.7 percent to 13.1 percent in 2020, up from 9.4 percent in 2019.

Another important indicator of profitability, EBITDA (earnings before interest, depreciation and taxes), increased strongly in 2020 following the decline in 2019. EBITDA, which was TL 21.9 billion in 2019 in the ICI Second Top 500, increased by 55.9% to TL 34.2 billion in 2020. This showed that in 2020 companies focused more on their main areas of activity and EBITDA profits.

The considerable increasing trend in operating profit and EBITDA is also reflected in the total pre-tax profit and loss. The ICI Second Top 500's total profit and loss before tax climbed by 90.2 percent in 2020 to TL 20.1 billion from TL 10.6 billion in 2019.

In the ICI Second Top 500, ordinary revenues and profits from other operations were TL 40.4 billion, and ordinary expenses and losses from other activities were TL 39.4 billion in 2020. The difference between these two items reveals that the ICI Second Top 500 generated 1 billion Turkish Lira in non-operating revenue.

Currently, the foreign exchange transactions of this size seem to have decreased profitability in 2020 as they were in 2019. Despite this negative aspect, the fact that the effect is rather minor indicates that SMEs have improved their ability to manage exchange rate swings.

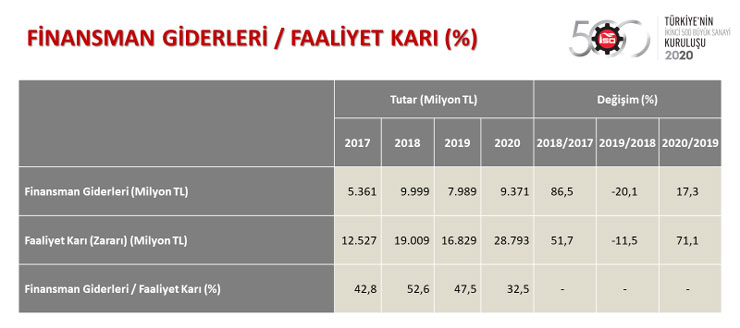

Financial expenses continued to be one of the main determinants of the profitability of industrial companies in 2020. However, as a result of the developments, single-digit loan interest rates applied for most of the year limited the increase in financing costs of the ICI Second Top 500. The depreciation of the Turkish Lira had a negative impact on financing expenses, which was less than expected.

Financial expenses increased by 17.3 percent in 2020, reaching TL 9.4 billion, while operating profits increased by 71.1 percent, reaching TL 28.8 billion.

As a result, the ratio of financing charges to operating profit fell from 47.5 percent in 2019 to 32.5 percent the following year, the lowest in recent years.

In short, ICI Second Top 500 firms devoted a lesser portion of their operating profit to finance expenses in 2020. Thus, they are provided with more favorable conditions to increase their profits and equity.

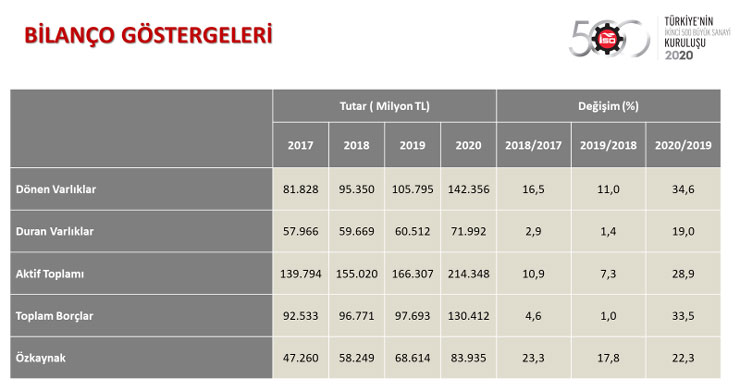

The balance sheet items of ICI Second Top 500 and the changes it has shown in the past three years reveal that the ICI Second Top 500 balance sheet growth was 28.9 percent in 2020. This high growth was fueled by increased total liabilities by 33.5 percent and shareholder's equity by 22.3 per cent.

In 2020, ICI Second Top 500 firms experienced substantial equity growth with the help of increased profitability, but they also demonstrated a faster borrowing trend than in prior years.

Even though the situation appears to be worse than in the previous two years, when debts grew much more slowly than personal money, the exceptional conditions of 2020 can be claimed to have had a significant impact in these developments.

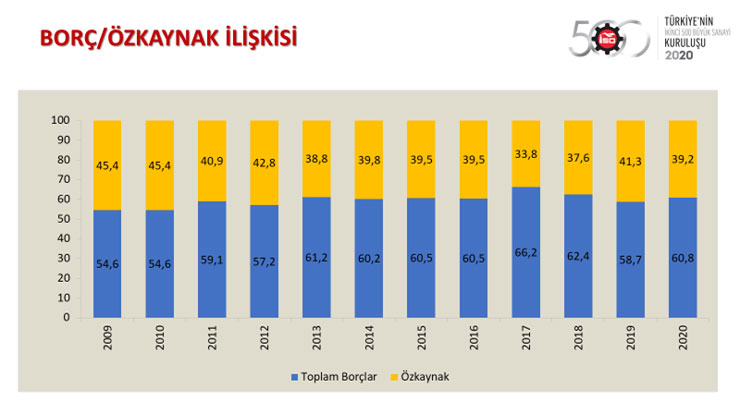

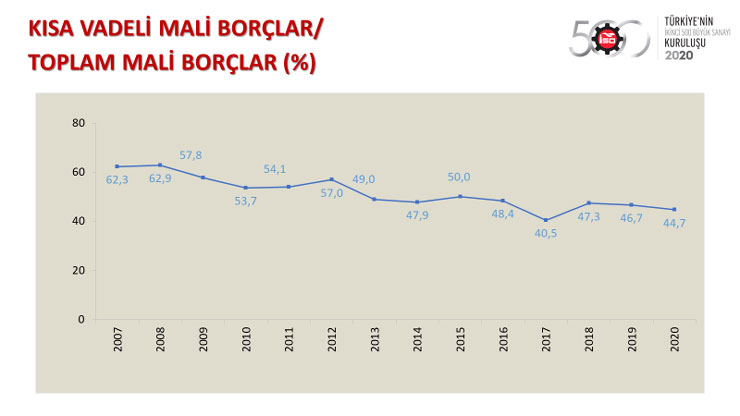

The debt/equity relationship of the ICI Second Top 500 companies shows that after two years of improvement, the debt to equity balance again progressed against equity in 2020.

While the share of equity in the ICI Second Top 500 was 41.3 percent in 2019, it decreased to 39.2 percent in 2020. The share of total debt rose from 58.7 percent in 2019 to 60.8 percent in 2020.

The image in question demonstrates that the deterioration in the debt-equity balance remains a persistent problem that industrialists must address.

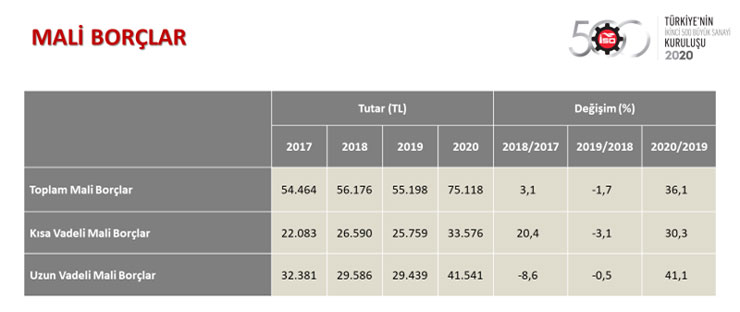

Borrowing and financial borrowing appear to accelerate significantly in ICI Second Top 500 in 2020. It is understood that the low-interest and medium-term loan support packages that were implemented in the post-pandemic period have encouraged borrowing. While financial liabilities rose by 36.1 percent in the same year, the increase in short-term financial liabilities was 30.3 percent, and the increase in long - term financial liabilities was 41.1 percent, more than in previous years.

Long-term liabilities increase faster than short-term liabilities, which can be seen as a positive transformation for the maturity quality of borrowing.

As a matter of fact, the share of short-term financial liabilities in total financial liabilities fell from 46.7 percent in 2019 to 44.7 percent in 2020. Strong credit support through the banking sector is expected to have contributed to this decline. The large portion of these loans being medium term has played a role in the improvement of the maturity structure of the financial liabilities.

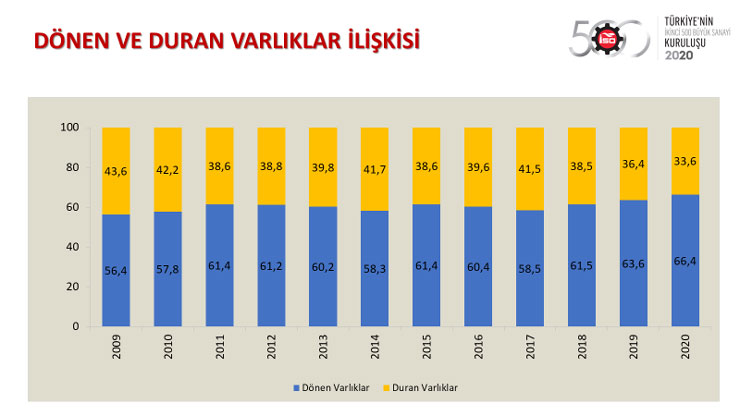

When we look at the relationship between the current and non-current assets of the ICI Second Top 500, it has been observed that the deterioration against non-current assets has continued to increase for the last 3 years. While, the share of current assets increased from to 66.4 percent in 2020 from 63.6 percent in 2019, the share of non-current assets decreased from 36.4 percent to 33.6 percent. This indicates that SMEs have spent a stable year in 2020 in terms of investments in machinery and equipment.

The deterioration, on the other hand, is thought to be caused in part by the fact that the entities in the companies' balance sheet have not been subject to revaluation for many years.

One of the issues that industrialists expect to find a reasonable solution in recent years is the transferable VAT receivables; these continue to be a serious problem for both ICI 500 and ICI Second 500 companies. This burden, as it may be recalled, for ICI Top 500, amounted to TL 12.4 billion, up 14.3 per cent in 2020. In ICI Second Top 500, the transferred VAT increased to TL 2.5 billion, up 31%, compared to the previous year.

This indicates that VAT receivables are starting to become a much heavier financial burden for companies in the ICI Top Second 500 league, as it is in the ICI 500.

In ICI Second Top 500, the number of profit-making firms climbed from 430 to 443, while the number of loss-making organizations declined from 70 to 57 in 2020. This makes the number of profitable businesses reach the highest number for the period 1998-2020. In the economic and financial conditions that emerged in 2020, companies focus on increasing their profitability. Support factors such as low-interest loan facilities seem to contribute to the increase in profitability.

It is noteworthy that, in terms of EBITDA, almost all (495 companies) of the ICI Second Top 500 closed the year with profit.

The industrial sector maintains its position as one of the most crucial fields for employment and qualified human resources. 2020 has been a special year especially in terms of business life. Due to the pandemic, the health of the workforce has become even a greater priority. Industrial companies have had to interrupt their activities intermittently.

Despite all these developments, the employment in ICI Second Top 500 has increased by 4.6 in the year 2020. Boosting employment in a troubled year such as 2020 reveals that the ICI Second Top 500 companies, as well as the ICI 500, make a strong contribution to employment.

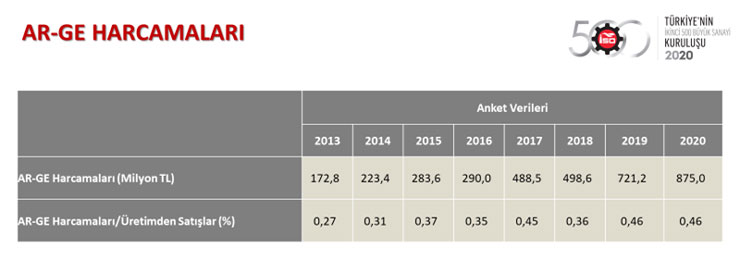

The number of companies performing R&D in the ICI Second Top 500 was 222 in 2020. Although there is a decrease compared to 2019, this number was the second highest ever measured. R&D activities are vital for the competitiveness of the industrial sector, and it is also an important finding that despite the challenging conditions in 2020, nearly half of the ICI Second Top 500 continued their R&D studies.

Despite the expectation of a rise, the number of organizations spending money on research and development remains below the targeted level.

And despite a decline in the number of R&D companies, the number of R&D expenditures of the ICI Second Top 500 rose to 875 million Turkish lira with the survey data. This figure indicates an increase of 21.3 percent compared to the expenditure amount of TL 721.2 million in 2019. Accordingly, it could be said that R&D expenditures have shown relatively rapid and positive real growth in 2020. Furthermore, R&D expenditures are growing stronger compared to the 4.9 percent increase in the ICI 500.

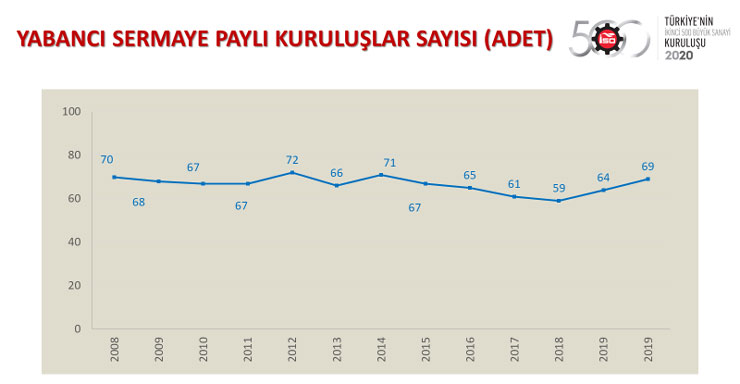

The number of foreign capital companies in the ICI Second Top 500 continues to increase. As you can remember, in 2019, the number of foreign-invested institutions increased by five, reaching 64. In 2020, the number of organizations with foreign capital shares increased by 5 to 69. So we went back to around 70 observed in the past years.

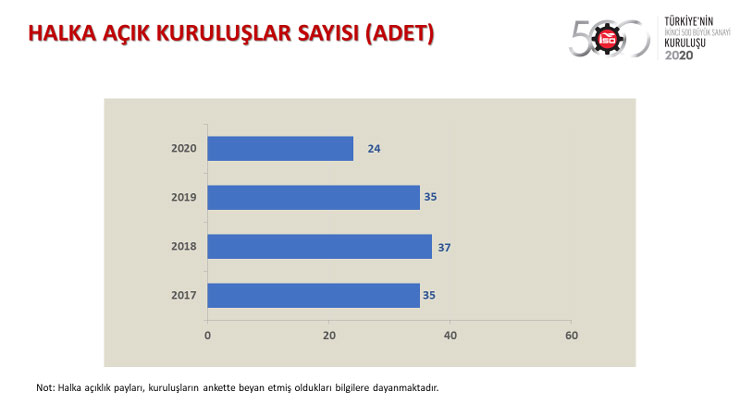

The number of publicly held organizations in the ICI Second Top 500 was 35 in 2017, the year the data began to be collected, and increased to 37 in 2018, and dropped back to 35 again in 2019, remaining unchanged. In 2020, the number of publicly-held companies in the ICI Second Top 500 dropped by 11 to 24.

The limited number of publicly-held companies makes it clear that the link between the industrial sector and the capital markets needs strengthening. This fact clearly points out the importance of supporting industrial companies in opening up to capital markets and raising funds from these markets.

When the ICI Second Top 500 organizations are ranked according to their relevant chamber, it is noteworthy that the Anatolian weight in the industry is increasing and its distribution in Türkiye has started to show a more balanced development.

Although the number of companies decreased in recent years, the biggest share still belongs to Istanbul Chamber of Industry (ICI) with 141 companies. This number was higher five years ago with 166. Istanbul is followed by the Aegean Region Chamber of Industry and Kocaeli Chamber of Industry with 40 companies each, while Gaziantep 38, Bursa 29, and Ankara 20 ranking at high levels.

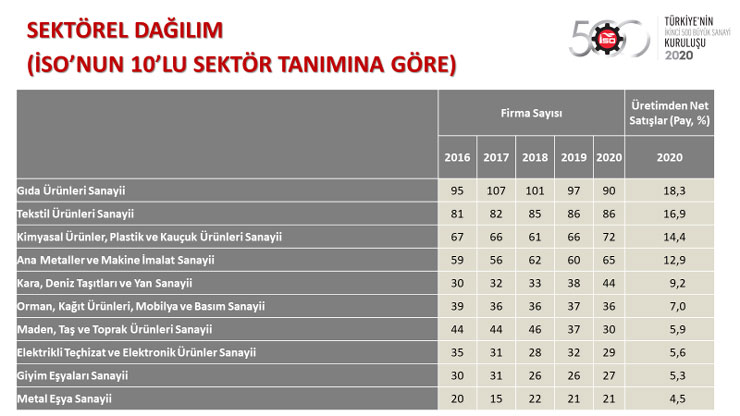

Considering the distribution of the ICI Second Top 500 according to the 10 sector groups created by ICI, it is seen that almost half of the companies in the ICI Second Top 500 are gathered in 3 sector groups. These are "food products industry" with 90 companies, "textile products industry" with 86 companies, and "chemical, plastic and rubber products industry" with 72 companies.

The three sectors in question also generate almost half of their production-based net sales according to 2020 data. In parallel with the number of companies, the highest weight in production-based net sales is in the "food products industry" group.

The most striking changes in the distribution of the industry compared to five years ago is that the number of firms increased by 14 in the "land, sea vehicles and sub-industry" group, but decreased by 14 in the "mining, stone and soil products industry".

In the ICI Second Top 500 ranking of 2020, the top 10 firms were ranked according to the size of their production-based net sales as shown in the table. According to this, "Murat Ticaret Kablo Sanayi A.Ş." took the first place in the ICI second 500 with a net sales of 578.9 million Turkish lira. It was ranked 487th in the ICI 500 in 2019. It was followed by “Metal Matris San. ve Tic. A.Ş.” in the second place with a very small margin and again with its production-based net sales of TL 578.9 million TL. Metal Matrix was ranked 103rd among the ICI Second Top 500 in 2019. The third company was the "RTM Tarım Kimya San. ve Tic. A.Ş." with TL 571.5 million. This organization was ranked 97th in the ICI Second Top 500 in 2019.